AFP-Exam-1 Practice Questions

Applied Financial Planning Certification Exam 1 (AFP)

Last Update 4 days ago

Total Questions : 117

Dive into our fully updated and stable AFP-Exam-1 practice test platform, featuring all the latest Canadian Securities Course exam questions added this week. Our preparation tool is more than just a CSI study aid; it's a strategic advantage.

Our free Canadian Securities Course practice questions crafted to reflect the domains and difficulty of the actual exam. The detailed rationales explain the 'why' behind each answer, reinforcing key concepts about AFP-Exam-1. Use this test to pinpoint which areas you need to focus your study on.

A client refuses to provide details about debt balances, tax returns, and monthly expenses but asks the planner to confirm whether retirement at age 55 is achievable. What should the planner do?

A retiree receives income-tested benefits and needs occasional withdrawals for vacations and home repairs. Which account is generally most efficient for withdrawals that do not increase taxable income?

A client says, “I want to retire comfortably as soon as possible.” Which response best reflects the financial planning process?

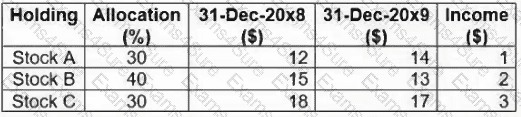

Consider the following information for a client's portfolio:

What is the annual rate of return for this portfolio?

Ram Patel, age 65, is meeting with his financial planner, Maria Romano, to complete a financial plan. Ram is retiring this year, and his company provides a defined benefit pension plan. Upon retirement, he has the choice of receiving $20,000 each year for 20 years or until death (whichever is earlier), or he can take $304,300, which is the commuted value at retirement. Ram has confirmed that he will be transferring the commuted value to a LIR

A.

After further discovery, Maria suggests that they utilize a 5% market rate of return and project the funds to last 25 years. What should Maria update Ram's projected annual retirement income to?Chris is a self-employed contractor discussing his retirement plans with his financial planner, Joseph. Chris is considering incorporating his business and drawing funds from his corporation to fund his retirement income, yet he wants to ensure it does not impact his business's financial position. What advice should Joseph give to Chris?

In 2019, Glenda, age 46, visited her financial planner to discuss her goal of retiring at the age of 65. Glenda had questions about whether she qualified for the maximum amount of CPP and OAS benefits as she had immigrated to Canada just 10 years earlier to take a job as a nuclear technician. What should her financial planner have told her?

Carla, a financial planner, is meeting with a long-standing client, Jonathan. Jonathan informs Carla that he is upset and disappointed with the negative returns experienced with his investment portfolio. After acknowledging Jonathan's concerns, what should Carla's first step be in addressing his complaint?

Richard pays periodic spousal support and child support under a written separation agreement. Which statement is generally correct?

Jimi and Macy, both age 26, consider themselves risk averse. After reviewing their budget with their financial planner, they discovered that they have a negative cash flow every couple of months due to their discretionary spending habits. What would be an appropriate strategy for their financial planner to recommend to the couple to manage their negative cash flow?