P1 Practice Questions

Management Accounting

Last Update 3 days ago

Total Questions : 260

Dive into our fully updated and stable P1 practice test platform, featuring all the latest CIMA Operational exam questions added this week. Our preparation tool is more than just a CIMA study aid; it's a strategic advantage.

Our free CIMA Operational practice questions crafted to reflect the domains and difficulty of the actual exam. The detailed rationales explain the 'why' behind each answer, reinforcing key concepts about P1. Use this test to pinpoint which areas you need to focus your study on.

RFT, an engineering company, has been asked to provide a quotation for a contract to build a new engine. The potential customer is not a current customer of RFT, but the directors of RFT are keen to try and win the contract as they believe that this may lead to more contracts in the future. As a result, they intend pricing the contract using relevant costs. The following information has been obtained from a two-hour meeting that the Production Director of RFT had with the potential customer. The Production Director is paid an annual salary equivalent to $1,200 per 8-hour day. 110 square meters of material A will be required. This is a material that is regularly used by RFT and there are 200 square meters currently in inventory. These were bought at a cost of $12 per square meter. They have a resale value of $10.50 per square meter and their current replacement cost is $12.50 per square meter. 30 liters of material B will be required. This material will have to be purchased for the contract because it is not otherwise used by RFT. The minimum order quantity from the supplier is 40 liters at a cost of $9 per liter. RFT does not expect to have any use for any of this material that remains after this contract is completed. 60 components will be required. These will be purchased from HY. The purchase price is $50 per component. A total of 235 direct labour hours will be required. The current wage rate for the appropriate grade of direct labour is $11 per hour. Currently RFT has 75 direct labour hours of spare capacity at this grade that is being paid under a guaranteed wage agreement. The additional hours would need to be obtained by either (i) overtime at a total cost of $14 per hour; or (ii) recruiting temporary staff at a cost of $12 per hour. However, if temporary staff are used they will not be as experienced as RFT’s existing workers and will require 10 hours supervision by an existing supervisor who would be paid overtime at a cost of $18 per hour for this work. 25 machine hours will be required. The machine to be used is already leased for a weekly leasing cost of $600. It has a capacity of 40 hours per week. The machine has sufficient available capacity for the contract to be completed. The variable running cost of the machine is $7 per hour. The company absorbs its fixed overhead costs using an absorption rate of $20 per direct labour hour.

Select ALL the true statements.

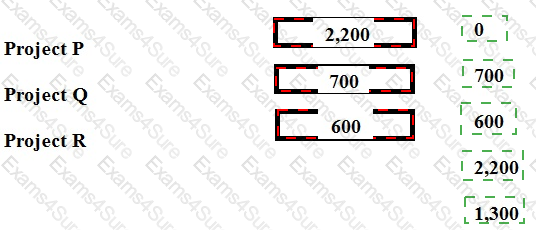

A company is choosing between three projects, Project P, Project Q and Project R using minimax regret as the criterion for the decision. The outcome from each project is dependent on future economic growth. If this is strong, returns will be P $5,000, Q $6,500 and R $7,200. If it is weak, returns will be P $3,500, Q $4,800 and R $4,200.

Place the correct figures into the table to show the maximum regret for each project.

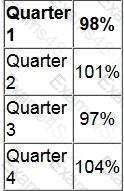

An analysis of past sales data shows that the underlying trend in a company's sales volume can be represented by:

Y = 50X + 625

Where Y is the trend sales units for a quarter and X is the quarterly period number.

The seasonal variation index values have been identified as follows:

The forecast sales volume in units for quarter 4 next year, which is period 14, is:

A company’s management is considering investing in a project with an expected life of 4 years. It has a positive net present value of $180,000 when cash flows are discounted at 8% per annum. The project’s cash flows include a cash outflow of $100,000 for each of the four years. No tax is payable on projects of this type.

The percentage increase in the annual cash outflow that would cause the company’s management to reject the project from a financial perspective is, to the nearest 0.1%:

Which of the following statements about total quality management are incorrect? Select ALL that apply.

A medium-sized manufacturing company, which operates in the electronics industry, has employed a firm of consultants to carry out a review of the company’s planning and control systems. The company presently uses a traditional incremental budgeting system and the inventory management system is based on economic order quantities (EOQ) and reorder levels. The company’s normal production patterns have changed significantly over the previous few years as a result of increasing demand for customized products. This has resulted in shorter production runs and difficulties with production and resource planning. The consultants have recommended the implementation of activity based budgeting and a manufacturing resource planning system to improve planning and resource management.

What are the benefits for the company that could occur following the introduction of an activity based budgeting system?

Select ALL the correct answers.

MDS is facing a temporary shortage of Material H which is used to produce all three of its products.

In order to maximise its profitability, which product should be manufactured first?

Changing to a just-in-time, from a traditional, manufacturing environment can affect cost accounting systems.

Which of the following statements is correct?

Which of the following explain why standard costing is less appropriate in the contemporary business environment?

1. In a continuous improvement environment standard costing can restrict the impetus to remain as cost competitive as rivals.

2. Fixed overhead variances are less relevant as fixed costs represent a decreasing proportion of total manufacturing cost.

3. In a just-in-time environment there are fewer costs to control.